Events this week could be mistaken for a cartoon if not so serious. And the cartoonish aspect magnified by clowns squirting lapel flowers in your eye every time something starts to make sense.

Events this week could be mistaken for a cartoon if not so serious. And the cartoonish aspect magnified by clowns squirting lapel flowers in your eye every time something starts to make sense.

The setup this week was for higher interest rates. This was an “auction week” for the Treasury, hawking $64 billion in new long-term paper. Ever since the deficit began to balloon in 1980, one of the easiest bets on the Street has been rates pushed up by Treasury selling. And Thursday’s news: claims for unemployment insurance last week free-fell by 32,000 to 300,000, a seven-year low. In previous expansion cycles a drop like that was enough to trigger an immediate rate hike by the Fed.

In perfect irrationality long-term rates fell within an inch of the 2014 low.

Most financial media say that rates have fallen because stocks have. There is some truth in that but not enough to matter. We live in a post-Copernican world: the sun does not revolve around the Earth, nor does the Earth orbit the stock market.

In the actual universe both markets are moving in response to the same external forces: the global economy is softening, the US is not accelerating and is unable to pull the rest, the whole shebang feeling the drag of deflation gravity, and the Fed alone among central banks is talking about tightening.

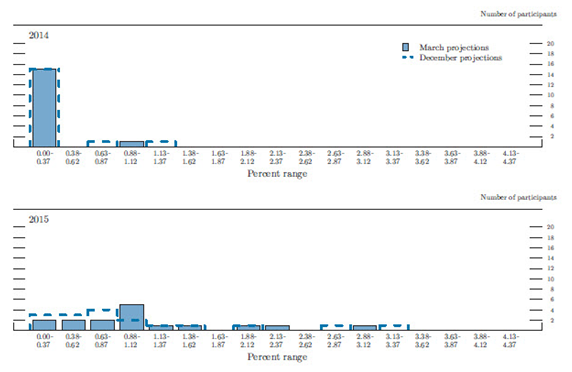

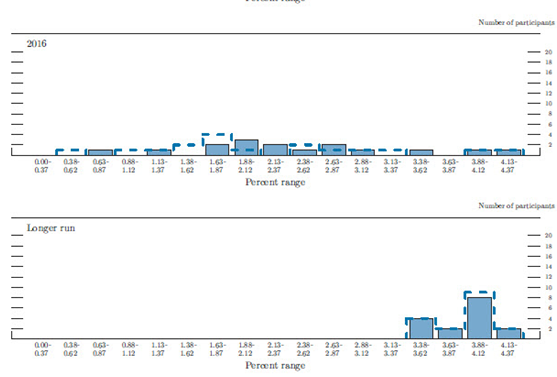

Enter clowns. The Fed’s post-meeting statement on March 19 included a chart of the governors’ and regional presidents’ forecast of the future Fed funds rate, “0%-.25%” since 2008. To considerable surprise in the markets the Fed seemed to pre-announce hikes next year to at least 1.00% and in 2016 to 2.00% or more — so surprising that markets withheld judgment. Good thing: the minutes of the meeting released on Wednesday cast Janet Yellen as Gilda Radner doing Emily Litella: “Nevermind.”

Market clowns want a transparent Fed. Every time the Fed tries for more transparency it wishes it hadn’t. The Fed is caught in a partially traditional predicament: it still needs to aid a fragile recovery unworthy of the name, but avoid creating new bubbles along the way and warn that if recovery gathers steam, then it will take away the punch bowl. The Fed funds forecast was entirely dependent on labor market acceleration not yet in evidence. Better to shut up than to sound like Donald Rumsfeld mulling known unknown known unknowns.

The Fed is stopping quantitative easing (QE3) as fast as it can. It accomplished little, if anything, and there may be a case — may — that it contributed to an overbought stock market. The Fed is supposed to “take away the punch bowl just when the party gets going,” but Chair Janet Yellen is correct that there is no party. To raise the Fed funds rate in these conditions would be trying to pull the tablecloth out from under the place-settings.

Housing is very close to stalling right now. Mortgage rates often do not rise tick-for-tick with the Fed, but they will this time. Tom Lawler finds the rate of home-ownership in collapse, at 63.3% lower than officially measured — and the lowest since 1965 and falling. The mania for asbestos banking wrapped tighter this week with the imposition of the first-ever-anywhere total-leverage requirement: 5% capital for all assets even if cash. Credit, or fireproof? Not both.

A strong catalyst for falling stocks and rates: China’s imports and exports both are sliding, and top officials began to break the news that its GDP would fail the reduced 7.5% target growth. Its yuan devaluation, like the yen, exports deflation.

The European Central Bank (ECB)continues to rattle an empty scabbard, threatening helpful stimulus five years too late. Half of Europe is in outright deflation. Marker: 5-year bonds of Italy and Spain have the same yields as ours. The deflation threat cancels their credit weakness.

Last clowns: striking a blow against sexism, the White House gave Kathleen Sebelius a last cigarette and led her to the bullet-pocked wall in the Rose Garden. Although the White House called all the ObamaCare shots, she got the blindfold. Her replacement, Sylvia Burwell, is very able (if on the all-southpaw team) and we might at least get some real numbers on ObamaCare revenue and expense.

———————————————————–

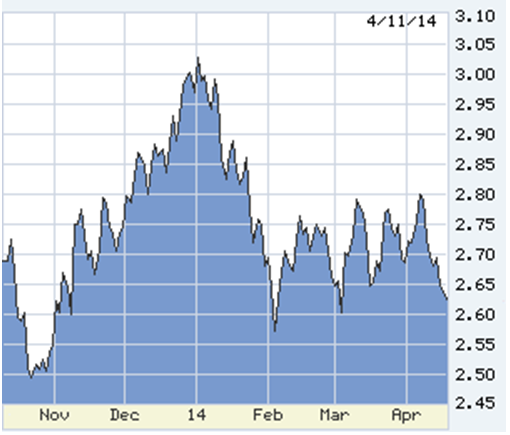

10-year T-note 90 days. The longer this trading range lasts, the more dramatic the breakout in either direction. Click on the charts below to expand.

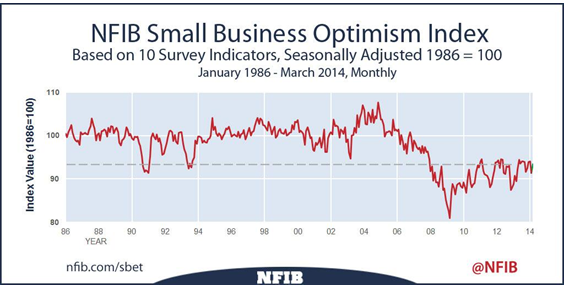

No real acceleration unless and until it includes small business.

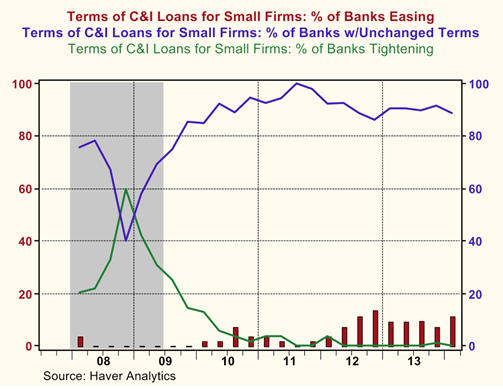

Credit terms, based on Fed surveys of senior loan officers. The fantastic tightening ’08-’09 is still in place.

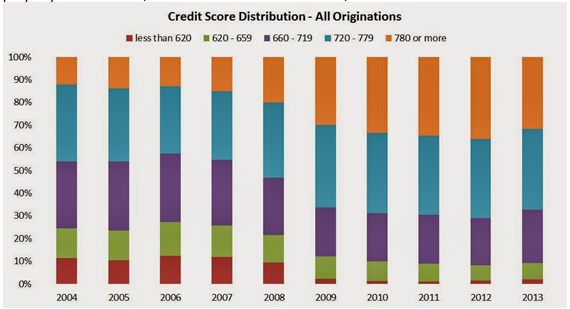

I’m okay with diminished mortgage supply (chart below) to those with sub-620 Ficos. But squeezing the 660-719 cohort is bad underwriting and suicidal for economic recovery. You can drop into that range with one late payment on a credit card. If properly underwritten, 620-659 should not be denied either.

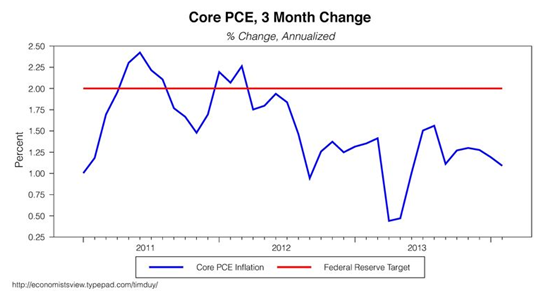

The Fed insists that inflation will soon rise to its target. Uh-huh.

Here is the beauty. This is the Fed’s forecast chart for the Fed funds rate as of the March meeting. 12 regional presidents each show as a single bar (half of whom are brilliant and capable, half should not be outdoors without a keeper), plus Congressionally confirmed governors (four in this rendering), and the Chair never expresses an opinion (so as not to spook markets, and to preserve the illusion of infallibility.

0 Comments