Markets are already quieting in front of two holiday-shortened weeks, after two calm-shattering ones.

Markets are already quieting in front of two holiday-shortened weeks, after two calm-shattering ones.

The five things unresolved, still on the table beside the turkey: what is the Fed up to? What is the support for an apparently accelerating US recovery? Does crashing oil help or hurt? Same for China’s slowdown? And Czar Vladimir?

Chair Yellen is doing a magnificent job. Has not missed a trick. Her post-meeting statement this week was perfection in elucidated obfuscation, simultaneously removing “considerable period” and saying that previous guidance was unchanged. Her most important aside: the Fed is prepared to lift off from zero before inflation rises to the Fed’s 2% target. Three self-important idiots felt the need to dissent (Fisher, Plosser, and Kocherlakota), confirming the need to find a way to remove the regional Fed presidents as voting members.

If job growth continues at this new 300,000 per month pace, the Fed will lift off by April, especially if wages change pace also. Even at the prior 200,000/mo pace the Fed will move this summer unless the economy slows a great deal.

Wage suppression

Why this strengthening recovery? Stick with the theory pushed here for a long time: US wages have undergone compression clear back to 1990 and may now again be world-competitive. The wage suppression has been accidental, not a work of government (as has repeatedly restored competitiveness in Germany), and terribly punishing to those with the lowest skills. But the painful phase may be passing. Thus the most flexible global economy does better than the others, over-managed or rigid.

Oil is a zero sum

Oil. The world burns about 90 million barrels per day. The price just fell $35/bbl, $3.15 billion/day, $1.15 trillion/year. That’s a lot of money, but not a lot when spread over the five billion people who burn most of it. Natural gas and coal were already down, so no collateral stimulus. The benefit of the oil price drop is quirky because of currency: oil is invoiced in dollars, so if you live with one of the many currencies devaluing versus the dollar, slim stimulus.

Oil is zero sum: producers lose what consumers gain. The US is tied with the Saudis and Russia for world’s-largest producer. Texas will feel a chill. So will global bankers to oil companies and petro nations, and markets addled by a shuffled deck.

Obnoxious sidebar: for hypocrisy nothing beats NY governor Cuomo banning fracking in the state. You’ll burn your share, but production is for lower castes, Dakota and Okie untouchables. The 1973 bumper sticker had it right for Yankees, whose energy bills are rising this winter (no new icky pipelines, no LNG terminals, no new transmission lines from Hydro-Quebec): “Let the *******s Freeze In The Dark!”

Overseas

China’s slowdown is more evident every day, although camouflaged by official statistics. In transition from a levitating, investment-led economy to a higher-order consumer-led one, slowdown is inevitable, imbalances taking a decade or more to wash out. But China’s levitation has always been predatory, pulling down Japan, Europe, and the US; a slowdown may well do less damage to wages in those places. China’s slowdown hurts the commodity producers who have fed its unsustainable explosion. It is well-nigh impossible to evaluate the effects of the ex-US slowdown on the US, but equally unlikely that there will be no effect on us.

Vladimir is not a new Czar. The Czars (and Soviets) were supported by secret police, and Vladimir is just a crooked cop, a gangland boss. You get to be capo di tutti cappi until you make a big mistake. Russia has lost 40% of its oil revenue; the remainder is enough to make oil-company debt payments, but all the grease is gone for the lesser mobsters. Combined with the ruble rumble, in a month stores will be empty of imported goods, the only things worth buying in a corrupt petro-state making nothing for itself.

Russians still bluster support for muscular nationalism. But they are thinking, Crimea and a smoldering Ukraine brought what reward? Beets, borscht, cabbage, onions, and potatoes… again.

—————————————————

10-year T-note in all of 2014. Downtrend still intact, but we’ll need more and more bad news overseas to keep going.

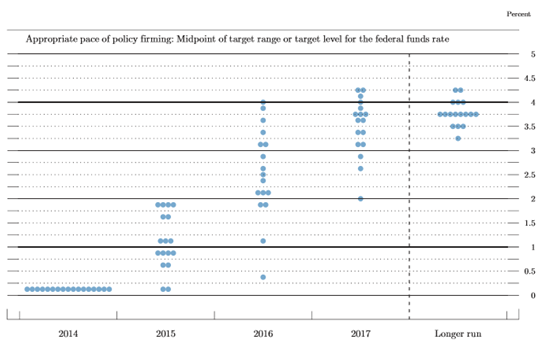

The Fed’s “Damned Little Dots.” Once each quarter the Fed Open Market Committee (governors nominated by the president and confirmed by the senate, plus 12 regional-Fed presidents) casts its dots to forecast the future altitude of the Fed Funds rate. Anonymously, but we can guess at four rockheads who want high, high, high. Throw those out, and you get a 1% rate one year from now. Fair guess. 2016… you’ve got to be one hell of an optimist to believe 2.00%-2.50%, for the first time since 2007 above the inflation rate.

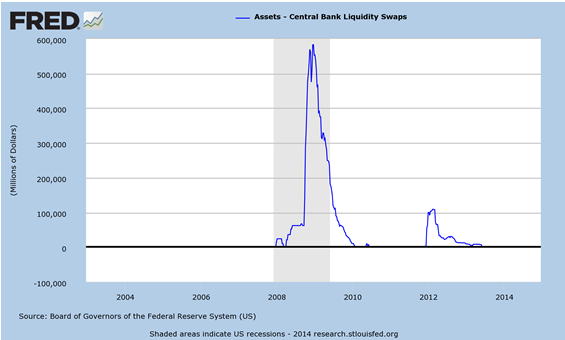

“Central bank liquidity swaps.” Huh? When there is panicked global demand for dollars, the Fed supplies bucks to foreign central banks in currency swaps. This operation gives the screaming bejabbers to gold bugs, Austrians, right-wingers, and even lefties like Warren. But it’s good, sound, depression-preventing business. It’s also by far the best real-time warning that the world is ending. Note immense spike at Lehman, and a lesser one when Europe looked gone. Data here one week old, but devaluations, oil, and ruble… no real alarm.

Just for fun, a ruble chart. Could not happen to a nicer bunch of people. On Monday the Russian central bank hiked its equivalent of the overnight Fed funds rate from 10.5% to 17% (which will just about stop its non-barter economy), and has spent a couple of billion dollar-quivalent in hard currency reserves — thus “stability” at about 60/dollar. However, fewer and fewer outsiders will accept rubles at all.

[hs_form id=”4″]

0 Comments