Calm down. Think it over, figure it out. Just because we see confusion and panic out there doesn’t mean we have to sign up.

Calm down. Think it over, figure it out. Just because we see confusion and panic out there doesn’t mean we have to sign up.

The media focus is on the stock market. If for no other reason than that, don’t pay much attention to the stock market. If it goes nuts in either direction, the authorities have to get involved, but we’re miles from that.

However, there is one useful hint from the stock market: for many months stocks have traded up on bad economic news, thinking that would mean the Fed staying on hold. The news has been awful — so bad that even if the Fed does lift off in September it will likely be an immaterial one-and-done. Now, the benefit of Fed on hold has been overwhelmed by something else, worse than Fed tightening.

We have several choices for that honor: Europe has entered a new, German-driven Greek deal which is ridiculous on its face. Greece will have new elections, but not really a government (or an economy). Pyongyang’s Fat Boy threatens war. Japan’s GDP “unexpectedly” shrank 1.6% in the 2nd quarter despite fantastic QE by the BOJ. A new, modest tsunami of currency devaluations ripple from Asia, too many to count.

At the center: China, of course. China drives everybody crazy because it’s the Saturday Night Live Liar of economic data. The economic/market upset underway would not be so troublesome if we had straight data and clear government intentions. Best I can figure, China began last year a multi-pronged effort to rebalance its economy toward consumption and open markets and away from state-driven investment and credit — and every effort has failed and left each sector in worse shape than to begin with. China used to have a stock market; now it doesn’t. Weaning from state credit has left it with more state credit outstanding and deeper reliance on it. The reputation of the leadership and Party has suffered accordingly.

China is not likely to land hard. If we’ve learned anything in the last decade, it’s that central banks can create relatively stable mountains of IOUs under their carpets. But the chain of events leading to broad market and economic upsets is in play anyway, China’s devaluation the immediate signal that global trade may be in trouble.

China’s consumption of commodities has crested, but the emerging-nation supply chain was calibrated for further increase. The emerging nations are also customers of China, and will buy less, increasing pressure on China. China is a customer of Europe and the U.S., and will buy less; hence so will they. In the last 25 years global trade has grown faster than GDP, everyone now everyone else’s customer. That global trade conveyor has made everybody rich, especially big corporations with global turnstiles enjoying unimaginable profit margins.

Ordinary cyclical oops-a-daisies are not a big deal, and that’s what this is likely to be. However, markets have the screaming bejabbers at the moment for fear of a reinforcing spiral driven by an incipient trade war becoming a currency race to the bottom. Even that is recurrent and recoverable. The part that’s not: we’ve never gone though an adjustment like this with so much debt outstanding, and deflation nearby.

Back to the Fed

Back to the Fed. Minutes of its meeting only three weeks ago were released Wednesday, and reveal the Fed properly uncertain then. Now, I assume jaw-dropped.

Exclusion is one way to get close to the heart of the matter. Things about the Fed that are not true: it did not miss its chance to lift off last fall, winter, or spring; if the world is too shaky now for liftoff, then lifting off earlier would leave it too tight now.

The Fed’s zero-percent policy and QE did not cause current difficulty — without its heroics 2008-9 we’d be living in caves. Nor the goofy plan to hike now so it can cut later.

The Fed does not have to lift off now, although it might just to shut up the irresponsible jackdaws and their financial creationism.

The only element of the U.S. economy flashing red is apparent “full employment,” and the need for pre-emptive liftoff. Nothing else is even amber. Keep it simple: the Fed doesn’t matter now.

The risk to the global trade conveyor exceeds all other risk combined.

——————————————————

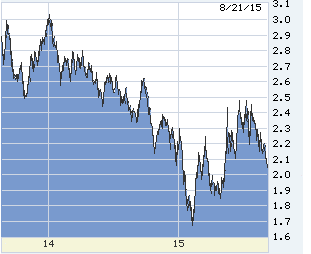

10-year T-note in the last week. Rising in fear of Fed minutes before Wednesday noon release, then reacting to the Fed’s uncertainty and a global-market air-pocket:

The 10-year two years back. Unless global markets rebound, and/or good news from China the next resistance is at 1.90% and mortgages below 4.00%:

Fed-predicting traders of the 2-year T-note still expect Fed liftoff soon. Comparing its yield to 10s says the Fed may lift off, but not for long and to no consequence:

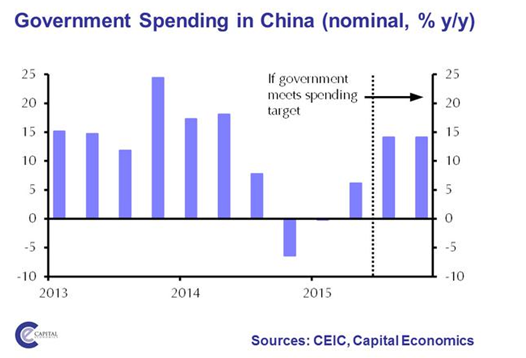

China apologists say that it has already re-opened the stimulus spigot after six months of failed rebalancing, and all will be well, its economy already turning up, surveys weak only because of the Tianjin explosion. Maybe. But even if so, the stimulus is just as unsustainable as before:

Productivity is the great mystery. Suggests to the Fed that the U.S. speed limit may be low, but everyone understands that the decline may be an error in measurement or implication in technology economies. Adds to Fed worry about very low unemployment and the prospect of wage increases beyond real productivity:

Here is the worry driving markets. A lot of other data supports this decline — especially falling activity at ports and among shippers:

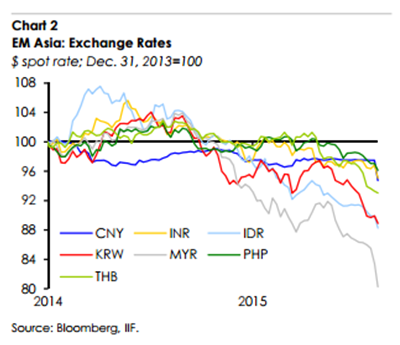

Simultaneously effect and cause: competitive devaluation in a race to the bottom. This chart is only one week old and out of date. Vietnam devalued this week for the third time this year, and South Korea’s won is off nearly 10%, partly due to Fat Boy. All values relative to the dollar. The US will slow in response to a unanimous external devaluation, and domestic inflation is impossible — as-was last month, import prices had fallen 10% year-over-year:

0 Comments