Here in the U.S. market participants are fidgeting and annoyed by the weather distortion of incoming data. Three housing reports of January-February activity were of course weak, but meaningless, the same for snapshots of manufacturing activity in New York and Philly-Fed. The longer we go without good information, the larger the market movement when the ear muffs and fogged goggles come off.

Here in the U.S. market participants are fidgeting and annoyed by the weather distortion of incoming data. Three housing reports of January-February activity were of course weak, but meaningless, the same for snapshots of manufacturing activity in New York and Philly-Fed. The longer we go without good information, the larger the market movement when the ear muffs and fogged goggles come off.

On Wednesday afternoon the Fed released minutes of its January meeting, and this line stopped hearts for a couple of hours: “A few participants raised the possibility that it might be appropriate to increase the federal funds rate relatively soon.” By nightfall everyone understood that “the few” were presidents of Regional Feds (Plosser, George, Fisher…) not in the majority, and the dimmest group in modern memory.

Wednesday’s sale of WhatsApp — 55 employees, $8 million invested in the startup, negligible revenue — for $19 billion begs the old question. If I had paid attention in school, might I have amounted to something?

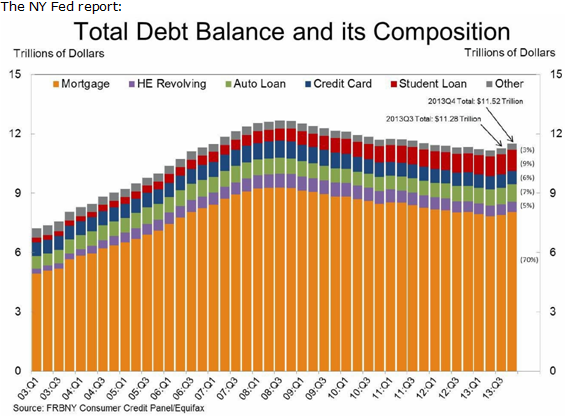

Dominant public commentary has the economy doing steadily better, and those thinkers seized on the NY Fed’s quarterly report of consumer credit. Deleveraging complete! Consumers borrowing again!

I am not one of the bears, just an agnostic made skeptical by the drumbeat of failed optimism in the last five years. And grumpy about poor analysis. The growth in consumer credit is in three places. Car loans, in which the subprime share has tripled from 2009, back over $150 billion per year. People will default on mortgages before the car, and cars are easier to repo than houses. Then student loans, balances doubling in the same five years, in the aggregate over $1 trillion, but inherently defensive. Tuition has risen like nothing except the cost of health care, and every student loan borrower by definition does not have the money, nor an asset to secure with a better loan (any mortgage is better — lower rate, longer term, deductible).

The third category: mortgage balances grew by a hair in the first quarter since 2008 Doomsday. However, the $9.5 trillion outstanding is a high-variety laundry basket. Deleveraging? The $1.5 trillion reduction in outstandings has been due entirely to foreclosure, not reflective of households still with loans. In the refi frenzies past, some estimates had almost half of refis switching from thirty to fifteen-year term. That is legitimate deleveraging, a steady reduction of principal owed. The minor increase in net-new loans is not sufficient to fund healthy housing markets, and tens of millions of households are still under water, or credit-wrecked altogether.

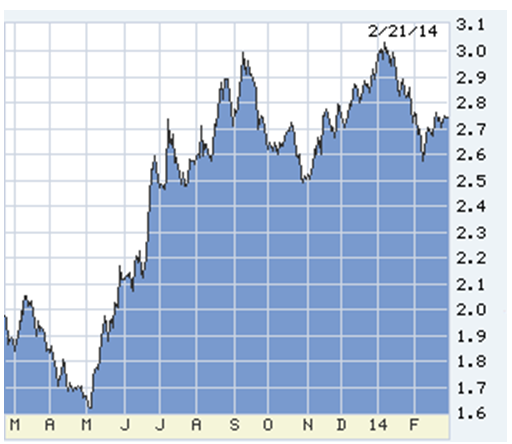

Until we get some springtime data, the economic-growth argument is a standoff. The 10-year T-note’s hold near 2.75% says it’s wary, if not about overall growth underway, certainly the persistent flirt with deflation. And overseas….

Japan’s last-ditch money-printing is not going as expected. In the 4th quarter of 2013 its economy grew 0.3%, one-tenth the forecast. Its trade has swung to huge deficit, $25 billion last month, which ordinarily would require foreign financing to balance accounts. Since no one outside will buy rice-paper JGBs, the BOJ must print to finance, which should drive the yen to new lows, helping Japan’s exports at the expense of everybody else. Japan in the next month plans another large fiscal stimulus simultaneous with a contrary increase in sales taxes from 5% to 8%. The world’s third-largest economy in counterproductive chaos is more than unsettling.

In China, just three things: the HSBC index of its manufacturing, kin to our PMI indices, at 48.3 fell farther into contraction in a seven-month slide. Forecasters still call for a 7% GDP increase this year. Third, despite emphasis in limiting credit the Peoples Bank of China said credit in January had risen at an 18% annual pace.

Kiev is a two-day drive from Sochi, the all-time Potemkin Village. Ukraine is aflame because Tsar Vladimir saw in its economic weakness a chance to snatch back an escaped province. In the old days, dangerous for us all. Now, the toothless decadence of both Russia and Europe leaves it a shabby, bloody, shadow-play of empires gone.

————————————————-

The NY Fed report: Click on charts to enlarge.

Maybe housing is just delayed, and will become the traditional, cyclical locomotive. Maybe it was on the way before a hard winter. Maybe.

10-year T-note in the last year. As in the copy above, non-distorted news can produce an explosive result in stalled markets.

0 Comments