Homes emerge from “underwater” in the past year

Negative equity, often referred to as “underwater” or “upside down,” means that borrowers owe more on their mortgages than their homes are worth. Negative equity can occur because of a decline in value, an increase in mortgage debt or a combination of both.For the homes in negative equity status, the national aggregate value of negative equity was $345.1 billion at the end of Q2 2014, down $38.1 billion from approximately $383.2 billion in the first quarter 2014. On a year-over-year basis, the value of negative equity declined from $432.9 billion in Q2 2013, representing a decrease of 20.3 percent in 12 months.Of the 44 million residential properties with positive equity, approximately 9 million, or 19 percent, have less than 20-percent equity (referred to as “under-equitied”) and 1.3 million of those have less than 5 percent (referred to as near-negative equity).Borrowers who are “under-equitied” may have a more difficult time refinancing their existing homes or obtaining new financing to sell and buy another home due to underwriting constraints. Borrowers with near-negative equity are considered at risk of moving into negative equity if home prices fall. In contrast, if home prices rose by as little as 5 percent, an additional 1 million homeowners now in negative equity would regain equity.“The increase in borrower equity of $1 trillion from a year earlier is evidence that things are moving solidly in the right direction,” Sam Khater, deputy chief economist for CoreLogic, said in the release. “Borrower equity is important because home equity constitutes borrowers’ largest investment segment and, as a result, is driving forward the rise in wealth for the typical homeowner.”

Negative equity, often referred to as “underwater” or “upside down,” means that borrowers owe more on their mortgages than their homes are worth. Negative equity can occur because of a decline in value, an increase in mortgage debt or a combination of both.For the homes in negative equity status, the national aggregate value of negative equity was $345.1 billion at the end of Q2 2014, down $38.1 billion from approximately $383.2 billion in the first quarter 2014. On a year-over-year basis, the value of negative equity declined from $432.9 billion in Q2 2013, representing a decrease of 20.3 percent in 12 months.Of the 44 million residential properties with positive equity, approximately 9 million, or 19 percent, have less than 20-percent equity (referred to as “under-equitied”) and 1.3 million of those have less than 5 percent (referred to as near-negative equity).Borrowers who are “under-equitied” may have a more difficult time refinancing their existing homes or obtaining new financing to sell and buy another home due to underwriting constraints. Borrowers with near-negative equity are considered at risk of moving into negative equity if home prices fall. In contrast, if home prices rose by as little as 5 percent, an additional 1 million homeowners now in negative equity would regain equity.“The increase in borrower equity of $1 trillion from a year earlier is evidence that things are moving solidly in the right direction,” Sam Khater, deputy chief economist for CoreLogic, said in the release. “Borrower equity is important because home equity constitutes borrowers’ largest investment segment and, as a result, is driving forward the rise in wealth for the typical homeowner.”

Highlights as of Q2 2014:

- Nevada had the highest percentage of mortgaged properties in negative equity at 26.3 percent, followed by Florida (24.3 percent), Arizona (19.0 percent), Illinois (15.4 percent) and Rhode Island (14.8). These top five states combined account for 32.8 percent of negative equity in the United States.

- Texas had the highest percentage of mortgaged residential properties in an equity position at 97.3 percent, followed Alaska (96.5 percent), Montana (96.4 percent), North Dakota (96.0 percent) and Hawaii (96.0 percent).

- Of the 25 largest Core Based Statistical Areas (CBSAs) based on population, Tampa-St. Petersburg-Clearwater, Fla., had the highest percentage of mortgaged properties in negative equity at 26.2 percent, followed by followed by Phoenix-Mesa-Scottsdale, Ariz. (19.5 percent), Chicago-Naperville-Arlington Heights, Ill. (17.9 percent), Riverside-San Bernardino-Ontario, Calif. (15.4 percent) and Atlanta-Sandy Springs-Roswell, Ga. (15.3 percent).

- Of the largest 25 CBSAs based on population, Houston-The Woodlands-Sugar Land, Texas had the highest percentage of mortgaged properties in an equity position at 97.5 percent; followed by Dallas-Plano-Irving, Texas (97.0 percent); Anaheim-Santa Ana-Irvine, Calif. (96.4 percent); Portland-Vancouver-Hillsboro, Ore. (96.1 percent) and Seattle-Bellevue-Everett, Wash. (95.4 percent).

- Of the total $345 billion in negative equity, first liens without home equity loans accounted for $180 billion aggregate negative equity, while first liens with home equity loans accounted for $165 billion.

- Approximately 3.2 million underwater borrowers hold first liens without home equity loans. The average mortgage balance for this group of borrowers is $227,000. The average underwater amount is $57,000.

- Approximately 2.1 million underwater borrowers hold both first and second liens. The average mortgage balance for this group of borrowers is $297,000.The average underwater amount is $77,000.

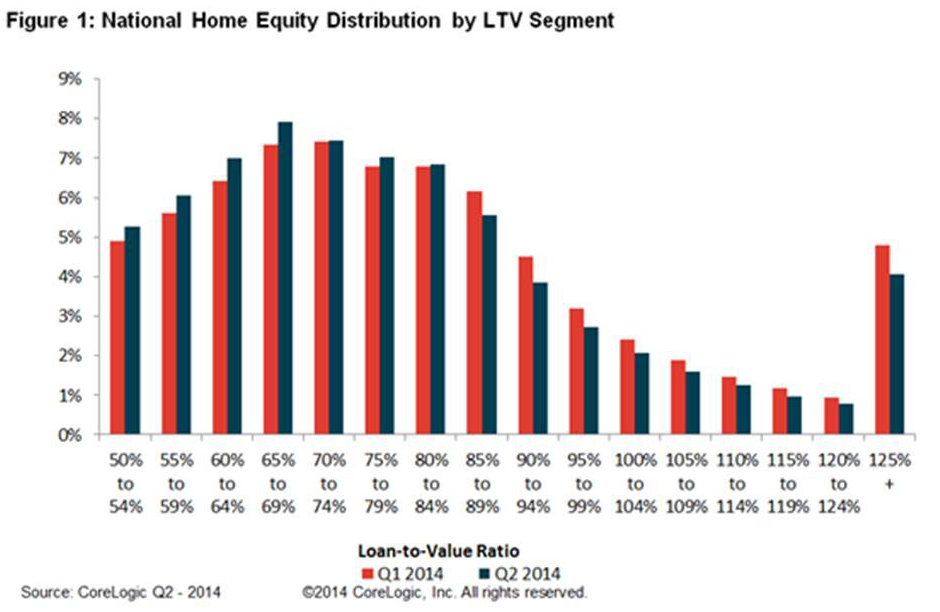

- The bulk of home equity for mortgaged properties is concentrated at the high end of the housing market. For example, 94 percent of homes valued at greater than $200,000 have equity compared with 84 percent of homes valued at less than $200,000.

0 Comments