The Great Recession officially lasted from December 2007 to June 2009 and had immediate and lasting negative financial impact on households and the broader markets. The economy bottomed out, crushing the real estate and stock markets, destroying $18.9 trillion of household wealth, and wiping out more than eight million jobs. Investors heavily invested in the stock market through investment and retirement accounts saw their portfolios wiped out almost overnight.

The Great Recession Created a New Population of Renters and a Need for More Affordable Housing

The demand for affordable housing rises during times of economic hardship, such as during a recession. As more people lose jobs and homes, the demand for affordable rental homes goes up. According to Harvard University’s Joint Center for Housing Studies, the renter share of all U.S. households jumped from 31 percent in 2004 to 35 percent in 2012, with that share projected to grow even more over the next ten years. Since the Great Recession, supply has outstripped demand for affordable housing, and that gap is currently growing with projections pointing to growth in the foreseeable future.

So, we know demand for affordable housing increases in a recession, but what is surprising about housing affordability trends in our current period of economic recovery and expansion is that the gap between demand and supply for affordable housing is widening. This gap can be attributed to a confluence of factors unique to this point in time in U.S. history, fueled by two disparate generations: Baby Boomers and Millennials. Affordable housing is attracting Millennial-age households and young families looking to minimize their carbon and environmental footprint by minimizing their living space. Retiring Baby Boomers are looking to extract equity from their family home and downsize to pocket the extra cash to fund a comfortable retirement lifestyle.

An Often-Overlooked Housing Option May be the Solution

Because of existing unprecedented demand for affordable housing, another recession will only make the gap between what owners and renters can afford and what is available to them wider, causing the number of low income renters to increase. I would say in no other affordable housing sector will this gap between supply and demand be wider than in the mobile home sector, a sector often overlooked and underdeveloped in real estate investors’ portfolios.

To make this sector even more intriguing, new mobile home communities just are not being developed. There are 8.6 million mobile homes in the United States, according to a 2013 U.S. Census Bureau report. “That number is not likely to grow…given restrictive zoning laws and the prohibitive cost of building a new [mobile home] park, meaning supply is static even as demand for cheap places to live is high,” wrote New York Times reporter Gary Rivlin on the topic in 2014.

With the demand for affordable housing constantly growing, investors can make a big difference in their communities and their investment returns if they invest in the right mobile home communities. The key is knowing where to look, what to buy, and how to improve the properties once you have them.

Doing Due Diligence on a Mobile Home Community

Because MHCs are inherently affordable and offer many benefits important to two of the biggest homebuying and renting populations in the market today, these developments are both recession-resistant and recession-friendly. Of course, investors must do careful due diligence when investing in such a property, since MHCs are unique in the housing sector.

Here are a few things to consider:

What is the actual Net Operating Income (NOI)?

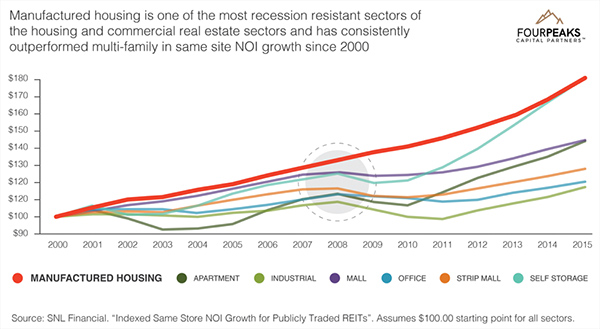

Since 2000, MHCs have offered some of the best NOI rates in the commercial real estate sector (see graph below). However, since many of these developments need some “TLC,” you must be very careful when evaluating a potential deal. Find out how the owner derived the current NOI and what they are using to base projections for the future.

What is the demand for affordable housing in the area?

What is the demand for affordable housing in the area?

Mobile homes are a great option for Baby Boomers and Millennials, but make sure that these populations are looking for housing solutions in an area before investing in an MHC. If they’re not hunting housing, you might be making a purchase that you cannot fully leverage. Carefully consider your market and the demand trends in the area.

How will you force appreciation, if necessary?

In many instances, we find that simply “upping the ante” in our community management has a nearly instantaneous effect when it comes to creating demand for residence in our MHCs. However, you must carefully evaluate the cost of making community-oriented improvements and the cost of vital improvements, such as rehabbing existing structures or replacing them, against local residents’ ability to pay higher prices for such upgrades.

Andrew Lanoie is the CEO of Four Peaks Capital Partners, a private investment firm based in Phoenix, Arizona, focused on alternative assets. Learn more at fourpeakspartners.com or email him directly at investors@fourpeaks.com.

0 Comments