Whether markets are resolving some of the uncertainties and frights leading to two weeks of chaos, or merely fatigued, they are settling down. Quiet is good.

Whether markets are resolving some of the uncertainties and frights leading to two weeks of chaos, or merely fatigued, they are settling down. Quiet is good.

The U.S. consistently shows more signs of “self-sustaining” growth. In the last seven years a false hope, but apparent now that the Fed can remove another set of its economic training wheels. The net of GDP revisions for the first six months of 2015: we are grinding along at 2.2% annual growth, which is probably the centerline of future prospects. Not accelerating, not fancy, but sustainable.

Housing in a long, slow recovery

Housing is in a long, slow recovery, unit sales rising about 6% annually, and prices perhaps 5%. Those numbers cannot pick up until incomes do, especially among the young, but at those levels would not contribute to inflationary overheating for several years. Or, given mortgage credit over-tightening, maybe ever. There is nothing too hot about this economy, with the possible exceptions of student and auto loans. Peanuts.

Inflation is the whole point of Fed operations. Its job is to intercept inflation (or deflation) before it gets going. The Fed’s models have over-predicted both GDP and inflation for seven-straight years, but that stopped-clock may at last have the correct time. Year-over-year core PCE inflation as of July had risen 1.2%, but in May plus .3%, June .1% and July .2% — the last three months account for half of the last year’s rise. If that’s a trend, the Fed has real reason to lift off, not just the yips to get off unnatural, bubble-inflating zero.

As the U.S. economy enters a normal realm, it’s entirely appropriate for the Fed to remove emergency and experimental ease. Two things hold it back: first the weird labor market mismatch, unemployment falling off the low end of the scale but very little growth in incomes. That’s relatively small potatoes, which will resolve themselves. If incomes suddenly take off, then the Fed will come harder and faster; if they stay low, the Fed can move very slowly.

The second Fed-retardant is huge. Or maybe not.

The outside world is a mess

The outside world is a mess. In many ways, all of it badly screwed up, and in important places — Europe and Japan — not at all clear how they get out of the traps they are in, no matter how energetic their central banks.

China is especially upsetting because it’s in obvious economic difficulty, but will not share honest numbers with the rest of us.

We tend to forget about slow-motion trouble spots, like Japan and Europe. The NYT reported this week that Japan’s declining population has resulted in 8 million abandoned homes. The BOJ’s QE has for a year bought Japan’s government debt at twice the rate of new budget deficit, which itself is half of Japan’s government spending. The BOJ now owns 27% of all Japanese government bonds. Here the Fed owns about 18% of marketable Treasurys and agency MBS, but stopped buying more than a year ago; at the BOJ’s current pace by 2020 it will own 65% of all JGBs. It will have to stop, but when, and to what effect no one knows.

And then there is China

Aside from the slow-rollers… China. The U.S. is the least trade-dependent economy of any major nation, only about 12% of GDP. Of that, China supplies 21% of our imports, and buys only 7% of our exports. But we have terrible measurement trouble. Trade used to consist of tangible goods, manufactured and raw, but “services” are the rapid growth category in modern economies. That’s what Google does. Apple sells tangibles, but implied sales of its intellectual property — innovation — are fantastically more valuable. Global employment compensation is every day more linked to and compressed by trade and instantaneous electronic price-discovery, brand new in just the last two decades and in that time accelerating at the pace of Moore’s Law.

We should all assume the Fed lifts off soon

We should assume the Fed lifts off soon. I hope in September, just to get the first step over with, and to make the Fed look like it knows what it’s doing. But I cannot imagine an inflation problem here or anywhere in a world like the preceding two paragraphs, and the Fed’s continuous rolling-over of its long-term Treasury and MBS holdings should keep mortgage rates low.

——————————————

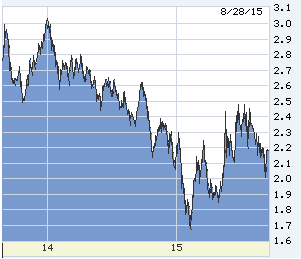

10-year T-note two years back. No matter how ugly it got in markets in the last two weeks, 10s could not break 2.00%, nor mortgages fall below 4.00%, and both yields began to rise by Tuesday even before markets had settled down.

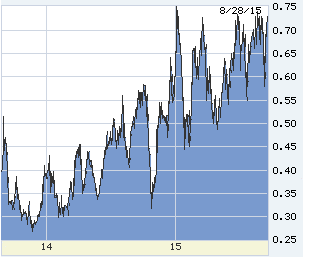

2-year T-note, two years back. 2s are the best predictor of the Fed (the fed funds futures market is worse than useless — wrong more often than right). The rising bottoms say the Fed is coming quickly, no chance for an open-ended stay at zero. On the other hand, the consistent top says markets believe clear through 2016 that the Fed will hike once or twice and done.

The best gauge of international financial distress is the Fed’s “liquidity swaps.” When demand for dollars goes wild in a meltdown of some kind, the Fed supplies dollars to other central banks — the onset of the Great Recession and then incipient collapse in Europe both plain in the chart. In 2015, still not a flicker of distress.

0 Comments