Last week was an exercise in perspective, stocks versus bonds and mortgages, and here versus over there.

Last week was an exercise in perspective, stocks versus bonds and mortgages, and here versus over there.

In a week with little new U.S. data (apartments hot, single-family not), bonds and mortgages stayed the same — which is remarkable given the performance of stocks.

The 10-year T-note could not break below 2.00%, mortgages just under 4.00%, but unchanged all through October while the Dow rocketed 500 points in the last two days.

These two markets usually trade opposite each other, stocks up on good economic news, bonds down in price and up in yield, and vice-versa on bad news. Good news should help corporate earnings and stocks, but any good news brings fear to bonds that the Fed will do something awful.

I have worked in or near credit markets for forty years, and like all colleagues regard the stock market as cognitively impaired and bi-polar, heavily overweighted to the manic side. Those people reciprocate, viewing us as depressed and void of imagination. How could these two pathologies join minds this week?

Bonds are right, and stocks don’t get it

The first stock up-burst coincided with European Central Bank chief Mario Draghi’s suggestion that he would expand its QE and perhaps drive euro-zone rates more deeply negative. The German 10-year fell in yield from 0.63% to 0.51%, pulling downward on U.S. 10s. Meanwhile stocks interpreted more central bank easing as economic stimulus good for them. Then Friday, the People’s Bank of China cut by surprise its overnight and reserve rates — more glee for stocks, but bonds holding.

Who is right here? My bias declared, of course bonds are right, and stocks don’t get it. In a normal world, big central bank stimulus would be good news for stocks, but this world is not at all normal. Unprecedented, fantastic stimulus by the ECB, PBOC, and BOJ has done nothing more than to hold up the economic floor and to buy time.

Europe is caught in its own wire and trenches, the euro a proxy for the Western Front in 1917. Germany profiteers and the weak cannot recover while the ECB merely maintains the meat-grinder — a situation unique to Europe, but real recovery impossible no matter what the ECB does.

China is different. It has hit its head on the ceiling of investment-led growth, and reforms attempted in the last year have all backfired. On Monday it reported Q3 growth slipping below its imaginary 7%, to 6.9%. Other indicators suggest a far deeper slowdown: as of September, industrial production is down 5.7% year-over-year, and fixed investment is off 6.8%.

More to the story: unadjusted for inflation, reported China growth was only 6.2%. China is in deflation, an upside-down adjuster. Factory prices have fallen there for 43-straight months. As China in some desperation tries to keep the machine going, it holds its export volume (down only 3.7% YTD) by predatory pricing, exporting its deflation and unemployment to the world while constricting its imports. Double damage.

Stocks misinterpret China stimulus even more than European. The weaker China becomes internally, the more harm it can do to the rest of us. I do hope that more people will understand that ongoing global economic mire has far more to do with the rise of China and its misbehavior than the financial crisis.

Why didn’t bonds and mortgages do better?

Okay, if it’s that ugly, why didn’t bonds and mortgages do better instead of just holding? Because of the great disconnect of our time: were it not for the rest of the world’s self-entanglement, the U.S.would be rocking. Fed-haters here include automatically in their screeds: “The Fed’s stimulus has failed to produce economic growth.” Horsefeathers. We have been growing so well that the Fed fears overheating, its leadership dying for an excuse to lift off, and might even be right.

Take some credit. No, not the Fed — take credit for U.S. flexibility, and endurance of pain. We have recovered from the Great Recession as nowhere else, our government dysfunctional throughout, because we alone could inflict millions of foreclosures and job losses, adjust and move forward. The rest of the world is politically and culturally stuck.

———————————————–

Larson’s cartoon captures the stock market’s difficulty separating true stimulus from false.

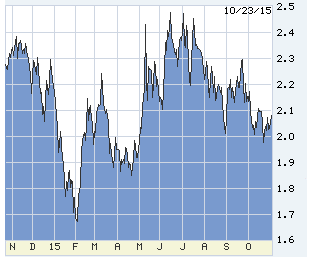

10-year T-note one year back. Stuck in a very narrow range which will not hold, but not likely to go very far whichever way it goes.

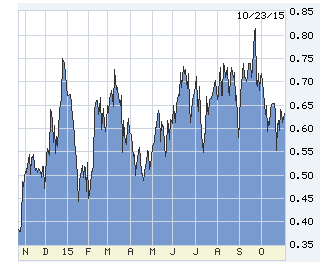

The Fed-predictive 2-year T-note. These traders get killed if they don’t see a Fed hike coming. Do they look scared?

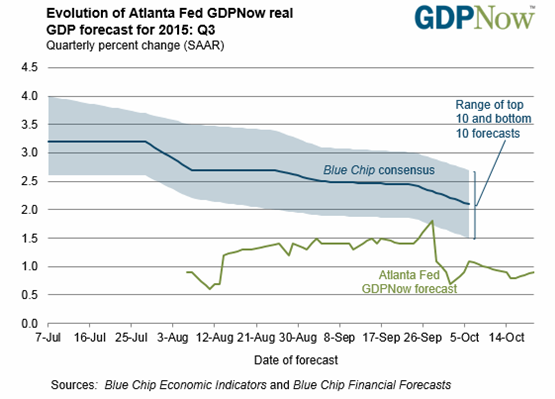

The Atlanta Fed’s tracker has been dead-on. We’ll be lucky if Q3 GDP is above 1%. If I were a Blue Chip Forecaster, I’d change jobs. The Fed itself has been just as bad.

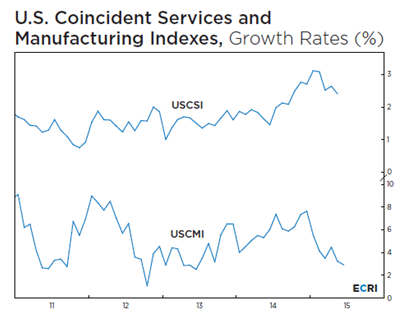

Now to the technical. The Economic Cycle Research Institute has the best recession-forecasting record of any outfit back to 1968. It notes that its leading index is now lower than the onset of five of the last seven recessions, but thinks “For the time being, the U.S. economic expansion is in a cyclically resilient phase where it is resistant to shocks that could tip the economy into recession… but a downturn that is poised to persist.”

ECRI detail since 2011. Manufacturing nosed over simultaneously with the dollar surge last winter, now joined by services. The declines are not yet serious, but have interrupted whatever momentum we had.

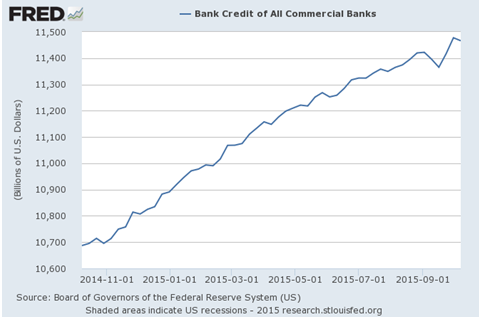

Nod to Paul Kasriel, retired Northern Trust Chief Economist but publishes his blog here. He detects a slowdown in bank credit, a kind of stealth tightening by the Fed. You can see the growth curve flattening during 2015, from rougly 8%, then to 5%, and in the last 45 days barely 2%.

0 Comments